GSTR-3B Filing Guide for February 2026 – Error-Free Compliance

GSTR-3B February 2026 – Ultimate Guide to Avoid Costly Errors

This Guide is written entirely from practical experience – the way i Personally handle GST compliance for clients every month. If you are preparing to file GSTR-3B for February 2026, Following this structured approach to avoid interest, penalties, and departmental nootices.

After years of handling GST Compliance for traders, services providers, manufacturers, and e-commerce sellers, I have seen that most mistakes happen because of:

- ITC mismatches

- Wrong tax liability reporting

- Ignoring interest calculation

Let’s go step by step ensure your February 2026 return is filled correctly the first time.

Understanding GSTR-3B & Due Date – February 2026

GSTR-3B Filing Guide for February 2026 – Error-Free Compliance

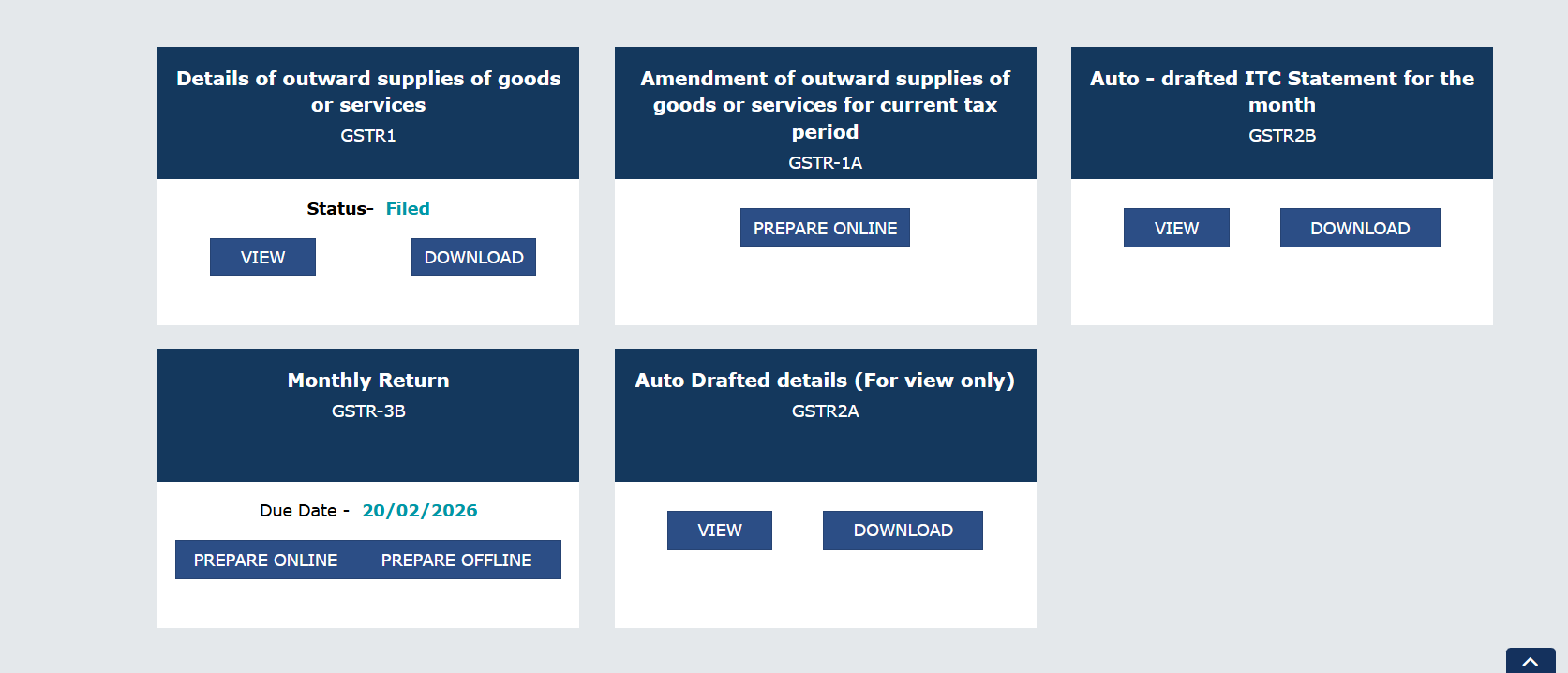

GSTR-3B is a monthly summary return filled through the Goods and Services Tax Network on the Official GST Portal

Due Date for February 2026:

- Regular Taxpayers – 20 March 2026

- QRMP Scheme – 22nd or 24th March2026 (depending on state category)

Professional Advice: Do not wait until the last date: Server slowdowns and payments failures are very common.

Pre- Filing 7-Point Reconciliation Checklist

Before filing any return, I ensure these checks are completed:

1. Sale Reconciliation

- Verify total February turnover as per books.

- Cross-check with GSTR-1.

- Adjust credit note properly.

If GST-1 and books mismatch, correct it before filing GSTR-3B

2. GSTR-2B vs Purchase Register Matching

Download February 2026 GSTR-2B.

Download February 2026 GSTR-2B.

- Match all purchase invoices.

- Identify missing ITC.

- Follow up with vendors where required

Best practice: Claim ITC only if reflected in 2B (Excepted RCM cases).

3. Reverse Charge (RCM) Review

Commonly missed liabilities

- Advocate Fees

- GTA services

- Security services

- Other notified categories

Ensure tax payment under RCM before claiming corresponding ITC.

4. E-Way Bill Cross Verification

For goods-based businesses, turnover must align with E-Way Bill date.

Mismatch increase scrutiny risk.

5. Previous Month Error Review

Check January 2026 fro:

- Short payment

- Excess ITC

- Reporting mistakes

Rectify adjustment properly in february.

6. Interest Calulation

Under GST provision

- 18% per annum for normal delay

- 24% for excess ITC utilization

Interest should not be ignored – the system tracks it.

7. Electronic Cash Ledger Check

Ensure sufficient balance before offsetting tax liability.

Table – Wise Practical Guide to filling GSTR-3B

Table 3.1 – Outward Supplies

This Section determines your tax liability:

- 3.1 (a) Taxable outward Supplies

- 3.1 (b) Zero-rated supplies

- 3.1 (c) Nill and exempt supplies

- 3.1 (d) Inward supplies under RCM

Verver mix exempt turnover with taxable turnover

Table 4 – Eligible ITC

Most scrutinized section

- 4(A)(5) – Regular ITC

- 4(B) – ITC Reversal

- 4(C) – Net ITC

Common ITC reversal include:

- Personal use

- Blocked credit Categories

- Non-payment within 180 days

Table 6 – Tax Payment

Understanding credit utilization order carefully:

IGST credit → IGST → CGST → SGST

Incorrect utilization can create technical non-compliance.

February 2026 Compliance Focus Areas

Recent compliance trend show:

- Increased automated matching of ITC

- Faster system-generated notices

- Higher scrutiny of sudden ITC spikes

If ITC usually high compared toto turnover, re-verify carefully.

Top 1o Mistakes to Avoid

- Incorrect taxable value

- Claiming ITC not reflected in 2B

- Forgetting RCM liability

- Ignoring interest

- Wrong Credit set-off

- No reconcilation

- Not reviewing previous month error

- Filling Without Management/client confirmation

- Incorrect export repoting

- Habitual late filing

Avoid these, and most compliance risks reduce significantly

My Structured Filing Process

Every month, we follow this internal structure:

- Finalize books by 15th

- Complete reconciliation by 17th

- Prepare draft working

- Obtain client confirmetion

- Download Preview

- Offset and Submit

Remember: GSTR-3B cannot be revised after filing.

Documentation to Maintain

Keep proper record:

- Sale Register

- Purchase Register

- GSTR-2B Copy

- ITC Working

- Interest Calculation

- Client Confirmation

Proper documentation protects you scrutiny or audit.

Practical Professional Advice

- Never rush filing without reconciliation.

- Always re-verify high-value invoices.

- Maintain consistent working format each Month.

- Plan tax Payment in Advance to avoid liquidity pressure.

GST compliance is not about date entry – it is about disciplined review and structured process control.

Can ITC be claimed if not in 2B?

Practically risk. Vendor follow-up is advised.

What is late Fees?

₹50 per date (₹20 per day for nil return)

What is excess ITC was claimed?

Reverse in next month’s Table 4(B) and pay applicable interest.

One thought on “GSTR-3B February 2026 – Ultimate Guide to Avoid Costly Errors”